(FICCI & PWC)

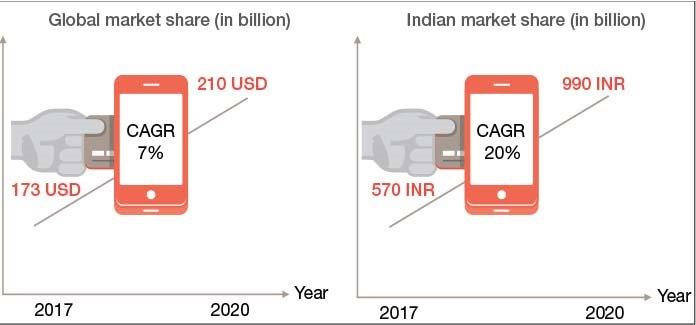

The security industry is a large and expanding area of the economy with an estimated global market worth of USD 173 billion. The private security industry in India, valued at INR 570 billion is also promising. The Indian industry is still nascent and is likely to see exponential growth both in terms of manpower employed, and market share due to rapid infrastructural and economic development, leading to an increased need for prevention, detection and protection of assets and citizens against criminal acts such as fraud, terrorism, theft, drug-related offences and violent crimes. Yet another factor adding to the demand is the increase in individuals joining the billionaire league and seeking private protection at all times.

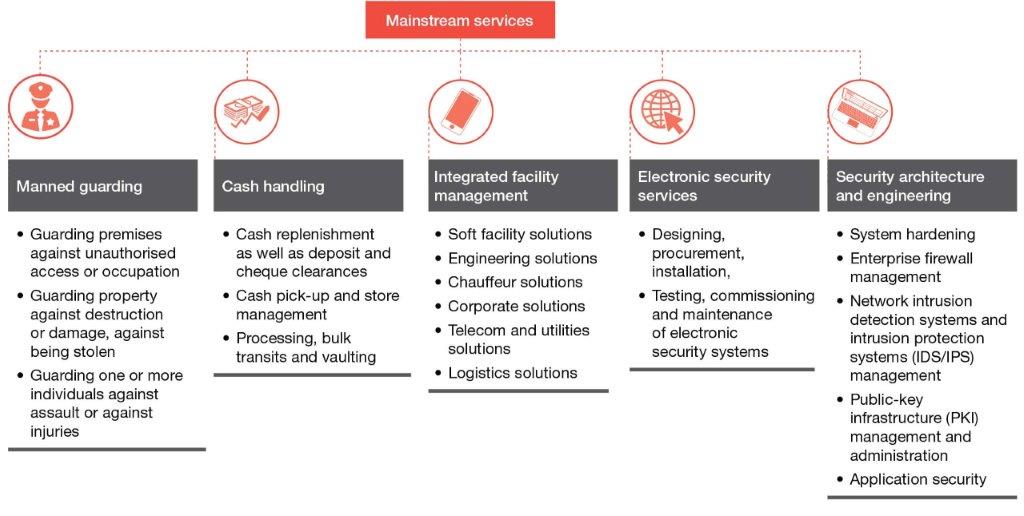

The private security industry is one of the largest employers in India and is continuously growing. It is employing almost 8.5 million people and has the potential to employ 3 million more people by 2020. Manned guarding continues to be the service line with maximum employment and is also the highest revenue generator for the private security industry, contributing to 80 per cent of the revenue, followed by cash services. Government policies like making guards and installing CCTV cameras in schools, ATMs, and various other locations mandatory have also accelerated the demand of the industry in the country. With a high level of advancements in technology, services like electronic security services, integrated facility management, and security architecture and engineering will see greater prominence in the time to come. This not only has the potential to improve the quality of services offered by security companies but may also prove to be a boon for the large workforce who will have the opportunity to up-skill themselves and progress to engaging employment conditions. With the passage of time, security companies have evolved from servicing only homes and businesses to servicing the government.

The rapid growth of the private security industry is both a refl ection of the inability of government security agencies to provide adequate security to private property and of the growing sophistication of the requirements of the private sector.

The rapid growth of the private security industry is both a refl ection of the inability of government security agencies to provide adequate security to private property and of the growing sophistication of the requirements of the private sector.

In the context of current policy and regulatory developments in the country, the private security industry will continue to play an important role. More investments coming into manufacturing and other related industries will not only trigger the demand for private security personnel but also compel the industry to adopt processes and practices in sync with international standards.

The contribution of this sector to employment generation in India is unique. Private security industry provides employment to a large number of rural youth, which otherwise would have remained outside the fold of formal employment.

– Dr. Sanjaya Baru

Secretary General, FICCI

However, as per the industry sources, 60 per cent of the security service providers still operate as unorganised, thereby keeping the sector price oriented, and amenable to unfriendly employment practices that make it difficult to monitor quality and compliance. The sector continues to be perceived by the work force as non-aspirational as people are unaware of career prospects and the benefits that can be achieved.

Technology integration is yet another challenge as it is widening the gap between the well-established players and smaller players in the industry. Most clients are now looking for technology-enabled security solutions which some of the bigger players in the industry already have; however, because of high capital and highly skilled manpower requirements, it is getting harder for smaller companies to keep up with the pace. Lack of quality manpower, high attrition rates and compliance requirements also continue to pose major challenges to the growth of the manned guarding security services market.

Government policies are changing the game quickly with important decisions being taken to overcome challenges such as revision in foreign direct investment (FDI) rates, re-categorization of security workers and modification in the minimum wages. However, the industry stakeholders are still of the view that more changes at the policy level and improved enforcement could help private security grow further and make the sector more viable for investments. Some key suggestions are creating a grading framework for private security players in the market and having a single window licence process.

Industry overview

Considering the growing demand for security services, security firms in India are seeking capital to expand their business. Some international players are also foraying into India to tap the potential of the industry.

Demographic characteristics

India’s competitive advantage has been its competitive wage structure and availability of manpower. A large number of youth within the age group of 15–19 fall below the poverty line as they drop out of formal education and have limited avenues for employment – majorly in regions including Bihar, Uttar Pradesh, Jharkhand, Madhya Pradesh, Rajasthan and Assam. They come to cities in search of better employment opportunities. The youth from cities, though, associate with the security industry with low aspirational value owing to lack of social security schemes, long working hours and poor working conditions. Nevertheless, the private security industry continues to be one of the largest employers in India. Over 90 per cent of this workforce consists of security guards who are at the base of the pyramid, with little to no relevant experience or expertise. They resort to working as security guards as the last option.

Recent policy initiatives

FDI rates: FDI in private security agencies (PSAs) has been revised through the automatic route to 49 per cent and through the Government approval route to 74 per cent.

Re-categorisation: In January 2017, vide a Gazette Notification, workers in private security have been re-categorized under the Minimum Wages Act, along with a modification in the minimum rate of daily pay. Security guards without arms have been recategorized as ‘skilled,’ and security guards with arms and security supervisors have been categorised as ‘highly skilled.’

Wage rate revision: The Central Government has also revised the minimum wage payable to employees of the ‘watch and ward’ sector to INR 637 per day effective April 2017. Stakeholders are of the opinion that more changes need to be brought in to make the sector more streamlined and profitable.

The private security industry has witnessed higher than 20 per cent growth in the recent past and is expected to continue to do so owing to rapid infrastructural and economic development. While its people have thus far been at the forefront of delivery in this service industry, technology and electronics are increasingly playing a strong complementary role. Hi-tech surveillance systems, remote sensors and biometric technologies may usher in a paradigm shift in the go-to-market strategy of private security players.

The private security industry has witnessed higher than 20 per cent growth in the recent past and is expected to continue to do so owing to rapid infrastructural and economic development. While its people have thus far been at the forefront of delivery in this service industry, technology and electronics are increasingly playing a strong complementary role. Hi-tech surveillance systems, remote sensors and biometric technologies may usher in a paradigm shift in the go-to-market strategy of private security players.

The private security industry had traditionally been dominated by un-organised players, and characterised by low-cost operations, missing corporate governance, low wages, and no statutory compliances or lack of employee welfare. Despite the advent of many global, professionally managed and progressive companies in this industry, un-organised players continue to retain a large market share by holding on to price-sensitive customer segments. Bringing such players into the ambit of regulation is the need of the hour. Tight enforcement of various labour welfare statutes such as minimum wages in accordance with the deployed skills, Provident Fund (PF) deductions, and mandatory enrolment in Employees’ State Insurance (ESI) and insurance plans is essential to ensure social welfare of the large manpower employed by the industry

– Pankaj Khurana

Partner, Government and Internal Security

PwC India

Industry structure

The private security industry, both globally and in India, has moved from its conventional services and diversified into newer fields. Although manned guarding has the highest employment rate and revenue share, rapid automation and technological advancements sees services like electronic security, remote surveillance, and security engineering and design gain momentum and chart a new line of mainstream services in the near future. The new-age security market has evolved from analogue to digital systems, with proliferation of features like intrusion detection, access control, surveillance and alarms, resulting in steady growth of the Indian electronic security equipment industry.

Moreover, security agencies have diversified into providing services like event security management, software and data security, and security consulting and training. India has opened its doors to large global festivals and sporting events with high footfall such as the FIFA U-17 World Cup, Indian Premier League (IPL), Global Citizen Festival and highly popular music concerts. Many more such events are likely to start in the near future.

The growth of such events has seen an increased need for event security management in India.

Software and data security is also a sought-after service, with NASSCOM envisaging that the Indian IT industry will grow to approximately USD 350-400 billion by 2025. The global cybersecurity market is expected to reach approximately USD 190 billion by 2025 from USD 85 billion in 2016, the main driver behind this growth being increased digitisation and increased smartphone penetration. The government’s initiative to make India a digital economy and the growing number of online financial transactions have accentuated the need for better cybersecurity.

With demand in the private security space increasing and with the increased need for quality and skilled resources, a tertiary sector quietly growing is that of training agencies, not only providing training for in-house employment but also servicing the industry at large.

Industry size and growth

Demand for security services across the country has grown enormously over the past 10-15 years. Going forward, by 2020, it is expected to become a INR 990 billion industry. While the global private security services industry is expected to grow at a compound annual growth rate (CAGR) of 7 per cent, the Indian private security services industry is expected to grow much faster at 20 per cent. The report states that the private security industry will generate around 3 million additional jobs by 2020.

Apart from revenue growth, the private security sector is also evolving in its employment practices. Some of the leading industry players are charting new standards in the industry with their keen focus on training and skill development of their people, establishing employee welfare funds, ensuring timely payment of salaries, and defining career progression paths for high-performing employees. A few companies that value the quality of manpower are also paying security men higher than the defined minimum wages to incentivise employee retention. Certain companies with an international presence are also introducing global best practices in their Indian operations such as on-demand continuous learning/ refresher training for their employees imparted through mobile solutions, job rotations and enhancing job definition to make the job more engaging for the individual.

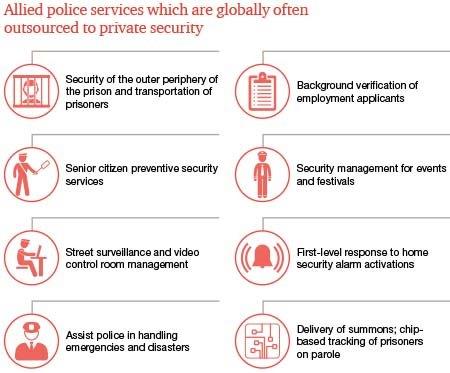

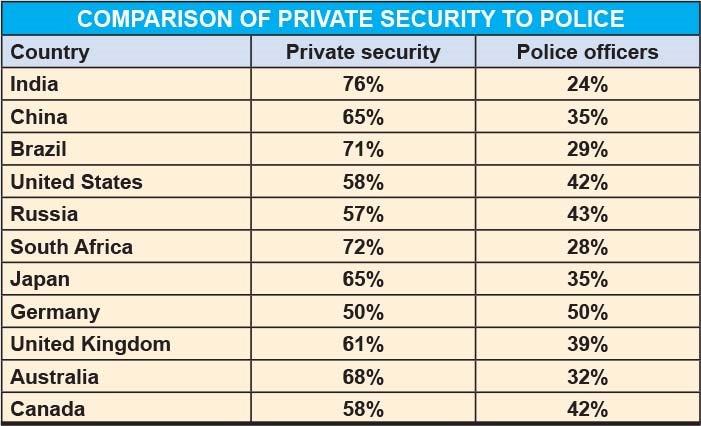

The private security industry in India employs 8.5 million people as compared to police services, where a meagre 2.2 million people are employed. As per the statistics published by Bureau of Police Research and Development, India in 2015 had actual police personnel to population ratio of 1:712 as against the sanctioned strength of 1 police officer for 547 people. A large workforce in the private security space can be utilised to make up for the low police to citizen ratio, with careful policy interventions to identify non-core areas of police and security functions that could be outsourced to such agencies – for example, senior citizen monitoring, outer periphery guarding of prisons and other government establishments, event security and police verification. This needs to be coupled with rigorous training and security compliances which these agencies may be asked to fulfil to get eligible for such business.

Investment in the sector

In June 2016, the government notified changes in the FDI policy with a view to making India more investor friendly and an attractive FDI destination. With these changes,16 international companies can have majority ownership in private security firms. Earlier, FDI in the security industry was capped at 49 per cent. Even though the government has allowed 74 percent FDI in PSAs, only 49 per cent is allowed under the automatic route, meaning no government approval is required. The change could make the sector more attractive to global security players.

Recent developments in India

In August 2017 the leading security service provider, Security and Intelligence Services (India) Ltd (SIS), was listed on the Bombay and National Stock Exchanges after raising close to INR 7800 million from an initial public offering (IPO). Another development is the imminent entry of yoga guru Baba Ramdev’sPatanjali Group into the private security business. With the tagline ‘Parakram Suraksha, AapkiRaksha,’ the security wing of Patanjali will be known as Ramdev’sParakram Suraksha Private Limited. It plans to recruit retired army personnel, paramilitary troopers and police personnel to ‘differently and professionally train’ them as private security guards.

Impact of recategorization of security workers

The Ministry of Labour & Employment, vide its Gazette notification dated 19 January 2017, re-categorised security industry workers under the Central Minimum Wages Act and modified the minimum rate of daily pay. This notification is a good move to make the industry more aspirational and attractive for the youth. Higher wages will attract better talent and enhance the quality of services provided by the sector.

The existing policy framework

It is important that robust regulatory mechanisms are in place to ensure the balanced growth of this industry to safeguard citizens’ welfare, and provide a fair and competitive operating environment to the industry. The private security industry in India is governed by the Private Security Agencies (Regulation)Act (PSARA), 2005. The Act provides for the regulation of PSAs and matters connected or incidental to the same. PSARA was enacted by the Parliament and extends to the whole of India, except the state of Jammu and Kashmir. The Act lays down regulations in terms of the following:

- Powers of the controlling authority.

- Licensing of PSAs.

- Eligibility for obtaining licence.

- Application for obtaining licence.

- Renewal of licence.

- Training requirements for private security guards and supervisors.

- Eligibility criteria for a person to become a private security guard.

The existing regulatory framework largely caters to the manned guarding portion of the industry but fails to provide concrete guidelines on cash services and electronic security services. Similarly, the guidelines do not cater to the procurement and maintenance of arms and ammunition required by private security guards.

Apart from PSARA, various other Acts including Minimum Wages and Payment of Wages Acts, Industrial Dispute Act, Contract Labour Act etc. impact the industry.

As states have the discretion to frame their specific rules based on the broader guidelines defined by the Central Model Rules act, 2006, a number of different procedures and compliances exist for companies operating in various states, resulting in greater procedural overheads. This is acting as a barrier to expansion for some regional PSAs. Each state has separate requirements for police verification, different timelines for processing the requests etc.

Many industry experts voiced an urgent need for a single window for the acquisition and renewal of licences, which would help in improving ease of doing business in this sector.

Stakeholder view on policy

Single window process: A uniform act governing licensing and other rules adopted across all states will greatly facilitate the ease of operations and may increase compliance with the regulations. Until this happens, a single window system for the submission and processing of applications for licences, renewal of licences etc., would prove to be useful. A central web portal could be useful to disseminate updated information amongst all stakeholders as well as faster processing of applications/ licence renewals.

Licensing norms: It is important to introduce a single licence for an agency operating in multiple states in contrast to obtaining state-wise licences, as is the case currently. Besides, the existing policy framework does not define what to do after the agency’s licence is cancelled due to an incident concerning a security guard, particularly with respect to existing service contracts that the agency may have with other customers. Thirdly, a valid police verification certificate of PSA directors in one state may be accepted and validated in other states as well to save time. Other challenges faced while acquiring licences at the state level include cumbersome documentation processes, long time lines to procure licences (varies from six months to two years), complex and time-consuming background verification processes, and no clear communication of reasons if applications are rejected.

Amendment of the Arms Act, 1959: There is no provision in the current act for an agency to procure the required weapons and then train its employees to use them.

Private security for allied police services: Given the low police to people ratio in India (one police per 720 people), PSAs can play a big role working along with the police for providing allied police services, however, this needs the backing of robust policy reforms.

Improved enforcement needs: The existing policy needs to be improved to cater to noncompliant or unlicensed agencies, default scenarios etc.

Employee viewpoint

Various reforms are essential to safeguard the interests of the manpower employed in the sector. A uniform classification for skilled and unskilled manpower may be followed by all states to allow mobility to employees. Presently, various states classify security guards under different brackets, thereby directly affecting the wage structure and the quality of manpower. Given the nature of the industry, the policy should also mandate provisions to provide insurance, better medical and wellness facilities, and the importance of self-defence and protective laws for guards. The right to detain a subject hampering security should also be permitted. The policy should provide Gmore emphasis on training of security guards.

Customer viewpoint

Given several complaints of behaviour issues of a guard, there are demands for aptly trained guards filled with professionalism. There is also a need to increase the number of women in this industry and provide them with the required physical training.

The workforce employed by PSAs lack in training and code of conduct in comparison with those by government agencies. Private agencies often do not have adequate training facilities for their manpower. Moreover, government agencies provide better benefits and perks.

Policy-level challenges

Amendment to PSARA, 2005

Changes in FDI limit

as per PSARA, an Indian should hold a majority of stakes in a company, and therefore, the decision to lift the FDI to 74% contradicts it. The Act needs amendment to align them. A company, firm or an association of persons shall not be considered for issue of a licence (for security agency) under this Act, if it is not registered in India, or having a proprietor or a majority shareholder, partner or director, who is not a citizen of India.

Absence of a clause on detainment

The current Act does not provide any authority to a private security guard to detain any suspicious person. However, in some developed economies, a security guard can officially withhold a person in case of any cynicism.

Presence of multiple regulations at the central as well as state level

The current regulatory framework necessitates obtaining a separate approval at the state level for licences. This acts as a barrier to the operations for different PSAs. Different states have different requirements for police verification and different time lines for processing requests. Therefore, various industry experts have proposed having a single window for acquiring relevant licences.

Ambiguity on the status post cancellation of licences

There is no clarity on the status of an agency in case its licence is revoked or the operating license renewal process is not completed in time. In such scenarios the agency may be permitted to perform its existing contracts till renewal, provided there is no issue raised by the controlling authority as part of the renewal process.

Challenges pertaining to the Arms Act, 1959

The PSARA has no clear definition on arms as well as armed security personnel. If the PSARA is read in conjunction with the Arms Act, 1959, then according to the Arms Act, 1959, arms can only be procured by an individual. This leads to the conclusion that PSAs cannot procure arms and distribute them among their guards. Also, as per the Arms Act, 1959, firearms cannot be used beyond the territory issuing the firearm which pose huge challenges for the industry.

Industry speaks – Operational challenges

Unhealthy competition in the private security market

Low prices of services, coupled with non-compliance with regulations have been the operational mode for some un-organised players. Some players underbid a tender to secure order and that leads to poor delivery of quality services. This practice has resulted in price-based competition instead of competition based on both price and quality. All these factors have posed a challenge to market players which are known to deliver quality services compliant with sector regulations.

Lack of required manpower/leadership/ skill sets

Skewed wage patterns for security manpower in India has proven to be a concern for PSAs in retaining required resources. Also, no defined career progression is in place for security guards. A PSA’s guard can grow to the position of a supervisor. The challenge lies not only in retaining manpower but also in attracting quality talent.

Further, due to ever-increasing competition in the market, costs need to be decreased by reducing manpower.

A challenge also exists with regard to trainers/ supervisors available in the industry. Based on research, it was observed that for about 1 lakh of security personnel, the industry has about 1,000-1,500 supervisors, which clearly shows the dearth of management personnel for the private security sector.

Issues related to licences

Not only is there ambiguity in the procurement of both state and centre level licences, but the complete process of procuring these licences is complex. A single window for the procurement of licences by deploying a web portal linked with PSARA portal is advisable.

Low margins

As per the survey conducted across major PSAs, ‘low margins’ was a common issue reported by these agencies. According to PSAs, the industry is already under stress with regard to cash flows owing to delays in payments from clients. On the top of that, GST, which the agencies claim is good for the industry, has impacted working capital. Therefore, there is a need to lower GST rates for PSAs as they are just the provider of manpower services and play the role of middlemen.

Less innovation and growth

This industry is still unable to fully harness the strength of technologies such as analytics, IoT, sensors, CCTVs and central command centres. According to an industry expert, this sector should be a mainstream component of the infrastructure sector and both the sectors should grow in parallel.

As a solution PSAs should collaborate with technology companies to develop solutions that offer the benefits of remote surveillance technologies, thus reducing manpower costs.

Way forward and recommendations

Leveraging new-age technologies

It is evident that PSAs are facing a shortage of adequate and skilled manpower. In addition to that, rising cost of manpower is a reality. Also, there has been a rise in various adversities such as natural calamities, loss of classified information, cybersecurity concerns and terrorist activities.

This has led to a demand for integrated solutions such as CCTVs and alarm systems.

Automated fire alarm systems including smoke detectors; gas, flame and heat detectors, and indication panel for fires; as well as integrated and automated home security solutions are some of the most significant requirements today. For a subscription fee, PSAs could take up the task of installing and maintaining such surveillance equipment, setting up of manned control centres and responding with a team of security staff and incident handlers.

Digitisation has made proactive monitoring of suspicious activities possible by informing concerned stakeholders via the establishment of command centres. Technologies such as video surveillance, along with predictive command centres, can play a crucial role in the private security industry.

Going one step further, the security market can also leverage new-age security technology solutions such as IoT sensors, analytics, real-time connectivity and biometrics.

Corporate background check

Currently, big corporate houses hire background verification agencies to conduct investigations on employees’ background. PSAs have already ventured into this area and this has become one of its growth factors.

Public-private partnerships (PPP) – hybrid policing

The role of the private security sector can be strengthened with the support of the government policing brigade.

Also, the private security sector can contribute in places where it is difficult for the police to attend. This shall lead to surveillance at a granular level and prevent an increase in crime rates. Countries such as the US and Netherlands are already working on these policies. This has led to an increase in personnel in the private security sector.

Introduction of new legal frameworks

In order to support the public forces, there is a requirement to make changes in the currently available legal support mechanism. Legal provisions may be considered to cater to scenarios where private security guards may need to use a firearm in case of an assault, to defend himself or the people that he is hired to protect.

Improvement in training techniques and required funding mechanisms

The provisions of government incentives/ subsidies for quality training to the workforce of PSAs are highly appreciable. Some such schemes are in force through NSDC.

This helps in defining the career path of the workforce and rewarding the high performers. Induction programmes on technology need to be the prime focus for each PSA.

Single licensing system

one-stop solution and dedicated portal for licensing can ease out the process of licensing and automation.

Improvements in enforcement

Listing and periodical updating of all registered licensed PSAs on the web portal; listing of agencies whose licence was cancelled along with the reasons; and a logo or standardisation mark for PSARA licensed vendors could act as a visible compliance marker and help in building publicity and awareness amongst potential customers.